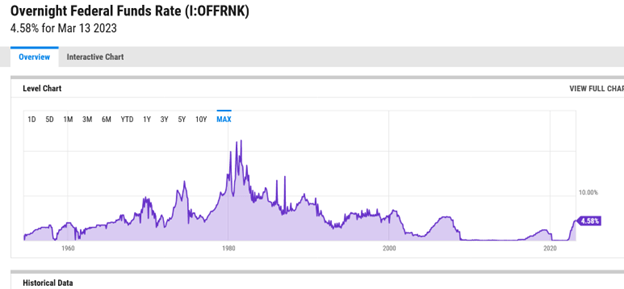

Interest rates have been low for a long time, and they’ve become part of the structure of our economy. Not since 2007 has the Fed overnight rate been as high as it is now, and for much of the time since the rate has been close to zero.

In some sectors, low interest rates have been used as a substitute for productivity gains, as in the housing market. We don’t have enough construction workers or existing housing, and we aren’t making widespread use of manufactured homes, but at least young people could get cheap mortgages.

In other cases we’ve used low interest rates as a substitute for industrial policy. Small cap companies (as represented by the Russell 2000), often have significant debt, and might go bankrupt with higher rates. But low interest rates effectively keep these companies afloat, and in many cases that’s a net benefit for the people. But we didn’t debate and vote on that, the Federal Reserve just arranged it.

And likewise with some social problems, such as student debt. You may have too much debt, but at least the interest rate isn’t 10%.

Beyond these, there are classically-recognized ill effects of raising interest rates: rising unemployment and bankruptcies, and decreased investment. So raising interest rates was going to cause harm; the only question is whether continuing inflation would be worse, as the Fed believes.

But I questioned whether something important—and unexpected—might break in the face of the Fed’s rapid increases. A year ago, the overnight rate was .08%; today it’s 4.58%, quite a jolt when you realize how deeply baked-in low interest rates are. And the Fed seems to believe it can continue to raise rates to 5% or even 6% without stepping on any rattlesnakes.

I was worried about higher mortgage rates leading to higher rents which could lead to a tipping point on homelessness. Imagine if the whole country had the homeless rate of, say, Portland. I was also worried about cascading bankruptcies among Russell 2000 companies leading to a recession.

And these could both still happen. But what I didn’t expect was a banking crisis, because banks generally benefit from higher interest rates.

But it does make sense. Bonds, especially US Treasury bonds, are a store of value used throughout the global banking system. And these bonds do not usually sit idle—they are used as collateral especially in inter-bank transactions.

When the Fed started raising short-term rates in April of 2022, this reduced the value of bonds issued before that time. Of course, the face value of the bonds is still secure, but the market value decreased significantly. When Silicon Valley Bank ran short of funds, they sold the Treasury bonds they had on hand, for a substantial loss. In normal times—post 2007, pre-2022—they wouldn’t have incurred such a large loss. The bank might still have had a problem, but the rest of the global economy wouldn’t have.

The Federal Reserve has undermined banking stability to the extent that stability depends on bond prices. And since all bond prices are correlated with US government debt, this problem isn’t limited to banks that are holding a lot of Treasury paper.

Bank runs and loss of banking liquidity are a real threat now. This could cause a global recession like the one of 2008-2009; in that light, maybe an inflation rate of 6% isn’t so bad. The urgent task of the Treasury Department and the world’s central banks is to quantify the reliance of banks on bonds for stability and liquidity. Some banks will likely have to close, at least temporarily.

The Federal Reserve and other central banks have clearly raised interest rates too quickly. Also, the single-tool method of fighting inflation needs to be scrapped; using interest rates alone has inherent risks to the larger economy. Temporary tax increases could be used, and the Federal Reserve (or the Treasury secretary) could be given the power to issue “stabilization bonds” in small denominations for US residents only. If we could issue $1000 7% bonds now (with a spread of maturity dates), and then just make the money raised disappear, then that would put a dent in M2. Naturally this might pose some temporary difficulties for banks, but I’m hopeful bankers will focus on the greater good.

Beyond those reforms, it’s time to question whether a private banking system subsidized and otherwise propped up by central banks and deposit insurance, and subject to more-or-less indifferent government regulation is working for us. Is this odd private-public model the right one for the 21st century?

Maybe after two banking crises in 15 years we should make a change?

https://ycharts.com/indicators/overnight_federal_funds_rate_market_daily

My prior comment belongs here more than on your 2016 post. Sorry about that!

LikeLike